")

As a content creator, you spend hours crafting engaging videos, blog posts, and social media content to share with your audience. But amidst all the fun and creativity, it’s easy to overlook one of the most important aspects of running your business — taxes.

Influencer and content creator taxes can feel daunting, especially when you’re new to being self-employed. The good news? Once you understand the basics, it becomes much easier to manage — and to minimize what you owe. This guide covers everything you need to know, from the taxes you’ll owe to how to file, write-offs to watch for, and common pitfalls to avoid.

1. Why Taxes Are Different for Content Creators

The role of content creator is relatively new — and the IRS hasn’t exactly made it simple. A few things make your tax situation unique compared to a traditional W-2 employee:

Multiple revenue streams. Most creators earn from ads, sponsorships, affiliate links, merchandise, and more. Each stream adds complexity and can come with different tax implications.

No withholding. When you work a regular job, your employer withholds federal and state taxes from every paycheck. As a self-employed creator, no one does that for you. You are responsible for setting money aside and paying the IRS yourself.

You pay both sides of the self-employment tax. At a regular job, your employer covers half of your Social Security and Medicare taxes. As a creator, you are both the employer and the employee — which means you pay both halves. More on that below.

You file quarterly, not just annually. Because no taxes are withheld from your payments, the IRS expects you to make estimated tax payments four times a year.

2. What Taxes Will You Owe?

If your business generates a net profit (income minus expenses), you’ll generally owe three types of taxes:

Federal Income Tax

Your federal income tax rate is based on your total taxable income and filing status (single, married filing jointly, etc.). The U.S. uses a progressive bracket system, meaning different portions of your income are taxed at different rates. Everyone who earns above a certain threshold must file a federal tax return, even if they owe nothing.

State Income Tax

State income tax rates vary widely. Some states — like Florida, Nevada, Wyoming, and Texas — have no state income tax at all. If you live in a state with income tax, you’ll owe it on top of your federal obligation.

Self-Employment Tax (FICA)

This is the one that catches most creators off guard. Self-employment tax covers Social Security (12.4%) and Medicare (2.9%) for a combined rate of 15.3% on your net earnings.

When you work a W-2 job, your employer pays half of this — 7.65% — and you pay the other 7.65%. As a self-employed creator, you pay the full 15.3% yourself. The silver lining: 50% of your self-employment tax is deductible on your federal return.

Example: If your net income is $50,000, you’d owe $7,650 in FICA taxes alone ($50,000 × 15.3%) — on top of your regular income tax.

Do You Need to Pay Taxes at All?

Whether you owe taxes depends on your net income — that is, your revenue minus your deductible business expenses.

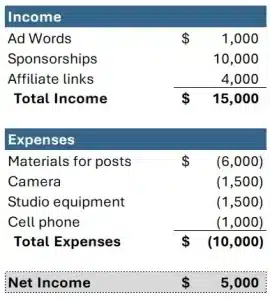

Example: Say you earned $15,000 last year ($1,000 from ad revenue, $10,000 from sponsorships, $4,000 from affiliate links). You had $10,000 in business expenses. Your net income is $5,000 — and that’s all you’ll owe taxes on.

If your expenses equaled or exceeded your income, your net income is $0, and you owe no tax, though you still need to file a return.

One important caveat: avoid operating at a loss for 3 out of 5 years. If you do, the IRS may classify your business as a hobby, which means you lose all your deductions and owe taxes on your full gross income.

3. How Much Should You Save?

A good rule of thumb is to save 25–30% of your income for taxes. Set that money aside immediately — treat it as untouchable until tax time. Consider keeping it in a high-yield savings account so it earns a little interest while you wait.

Most creators find that saving 30% covers the majority of their tax liability. Without this discipline, it’s easy to spend that money and end up scrambling when quarterly payments or April 15th rolls around.

4. Tracking Income & Expenses

Staying organized is the foundation of managing your taxes well. When everything is tracked consistently, filing becomes straightforward — and you won’t miss valuable deductions.

Set Up a Dedicated Business Bank Account

Open a separate bank account (and optionally a credit card) exclusively for your business. This single step makes tracking income and expenses dramatically easier and helps keep personal and business finances from getting mixed together — which is critical if you’re ever audited.

Use Accounting Software

A simple spreadsheet can work, but accounting software like QuickBooks or Wave (which lets you connect your bank accounts directly) makes the process much more efficient. The most important thing is to find a system you’ll actually use consistently and stick with it. Great news, we’ve created a free tool for you to use to start tracking immediately!

Good recordkeeping means you’ll have everything ready for quarterly payments, catch every deduction, and be able to fill out your Schedule C quickly and accurately at year-end.

5. Tax Write-Offs for Content Creators

Write-offs — formally called deductions — reduce your taxable income, which means you pay taxes on less. As a creator, you can deduct any expense that is ordinary and necessary to your business. Because your work is so closely tied to your personal life, the line can blur, but here’s a helpful test: if you purchased it specifically for your content, it’s likely deductible.

Common Creator Deductions

Equipment: Cameras, microphones, lighting, computers, hard drives, tripods, and similar gear can generally be written off in the year you purchase them. Major purchases like a vehicle used for business may need to be depreciated over several years. Save every receipt.

Software & Subscriptions: Adobe Creative Cloud, Notion, editing software, scheduling tools, stock photo subscriptions — all deductible if used for your business.

Home Office: If you regularly and exclusively use a dedicated space in your home for work, you can deduct it. Under the simplified IRS method, you deduct $5 per square foot, up to 300 square feet (so a 200 sq ft office = $1,000 deduction). Alternatively, you can deduct the percentage of your home used for your office against your total rent and utilities — this method often yields a larger deduction.

Internet, Phone & Utilities: The business-use portion of your internet, phone bill, and utilities is deductible.

Travel: Business-related travel expenses — airfare, hotels, ground transportation, and meals — are deductible. Keep records of each trip and note how it relates to your business.

Production Costs: Props, costumes, sets, location fees, and other production expenses are all fair game.

Contractors: If you pay editors, photographers, or other contractors to support your business, those payments are deductible (and you may need to issue them a 1099 — more on that below).

Note: Having an LLC does not unlock additional write-offs. A legitimate deduction is the same whether or not you have an LLC. What matters is whether the expense is ordinary and necessary for your business.

6. Quarterly Estimated Tax Payments

Because no taxes are withheld from creator income, the IRS expects you to pay taxes four times throughout the year rather than all at once in April. These are called quarterly estimated tax payments (Form 1040-ES).

Why Pay Quarterly?

While technically not required, skipping quarterly payments means the IRS will charge you penalties and interest when you file your annual return. Paying quarterly keeps you compliant and prevents an unexpectedly large tax bill.

How Much to Pay Each Quarter

Your quarterly payment depends on your projected annual income, filing status, and other factors. At a minimum, you’ll need to cover your FICA taxes (15.3% of net self-employment income), plus your estimated federal and state income tax.

A common approach: use an estimated tax calculator or worksheet to project your annual liability, then divide by four. Working with a tax professional can help you land on the right number, especially in your first year when you don’t have historical earnings to reference.

How to Make Federal Estimated Payments

Making the actual payment is simple:

- Go to the IRS Direct Pay website (IRS.gov)

- Select “Estimated Tax” and the current year

- Enter your personal information and estimated tax amount

- Enter your bank information and submit

Keep a copy of the confirmation for your records.

State Estimated Payments

Each state has its own system. Search “[your state] estimated tax payment,” and the first result will typically take you to your state’s government portal. You’ll likely need to create an online account to pay.

Quarterly Due Dates

- April 15

- June 15

- September 15

- January 15 (of the following year)

7. Do You Need to File a Tax Return?

Yes. If you made any income as a creator last year, you need to file a tax return — even if your net income was $0 after deductions.

Your Annual Return (Form 1040 + Schedule C)

Most creators file a standard personal tax return (Form 1040) with an additional form called Schedule C, which reports your business income and expenses. As a single-member LLC or sole proprietor, you do not need to file a separate business return — your business taxes are part of your personal return. The IRS treats single-member LLCs as “pass-through entities,” meaning your business income flows directly to your personal return.

Your Schedule C is straightforward if you’ve kept good records: you’ll list your total income, subtract your expenses, and report your net profit or loss.

Filing Your Return

You can file yourself using tax software like TurboTax, which walks you through your federal and state returns step by step. Budget around $150–$200 for software that handles both. Alternatively, a tax professional who specializes in content creators can handle your bookkeeping, quarterly payments, and annual filing for you.

Your annual return is due April 15, though you can request a six-month extension. Note that an extension gives you more time to file, not more time to pay. You’ll still owe any taxes due by April 15.

8. LLC vs. S Corp

Should You Form an LLC?

Yes — all creators should form an LLC. While your personal liability as a creator is generally limited, having an LLC makes your business look legitimate to brands you work with and to the IRS, and it helps you avoid being classified as a hobby. There are no additional tax filings required for a single-member LLC beyond the Schedule C you’d already file.

When Does an S Corp Make Sense?

If you’re earning more than gross ~$100,000/yr, or net ~$60,000, electing S Corp status may save you a significant amount on self-employment taxes.

Here’s how: as an S Corp, you pay yourself a reasonable salary (which is subject to full FICA taxes) and take the remainder of your profit as a distribution, which is not subject to self-employment tax at all.

Example: You earn $75,000 in net income. You pay yourself a $60,000 salary and take a $15,000 distribution. You pay full FICA taxes on the $60,000, but owe zero FICA taxes on the $15,000 distribution — saving around $2,300.

The tradeoffs: you’ll need to file a separate S Corp return (Form 1120-S), due March 15, and you’ll need to manage payroll for yourself. But above gross ~$100,000/yr, or net ~$60,000, the savings typically outweigh the administrative burden.

To elect S Corp status, file Form 2553 with the IRS by March 15.

9. Issuing 1099s to Contractors

If you paid a U.S.-based contractor more than $2000 in a calendar year (for video editing, photography, design, or any other work), you are required to issue them a Form 1099-NEC by January 31 of the following year.

When you onboard a new U.S. contractor, have them fill out a W-9 to collect their name, address, and tax ID. You’ll use that information to generate the 1099 at year-end. This requirement applies only to U.S.-based contractors.

10. Tax Timeline & Key Deadlines

Mark these dates on your calendar every year:

| Deadline | What’s Due |

| January 31 | 1099s issued to contractors |

| March 15 | S Corp return (Form 1120-S) — if applicable |

| April 15 | Personal tax return (Form 1040 + Schedule C) |

| April 15 | Q1 estimated tax payment |

| June 15 | Q2 estimated tax payment |

| September 15 | Q3 estimated tax payment |

| January 15 | Q4 estimated tax payment (prior year) |

Missing these deadlines can result in penalties — 5% of unpaid taxes per month for a late return (up to 25%), plus interest on unpaid balances.

11. Common Pitfalls to Avoid

Underreporting income. Report all income — from every platform, every sponsor, and every affiliate program. The IRS receives copies of your 1099s and can cross-reference them. Underreporting can lead to hefty fines.

Overclaiming deductions. Every deduction should be legitimate and documentable. If the IRS determines a deduction is fraudulent, it can tack on a 20% penalty on top of the taxes owed.

Missing deadlines. Late filings and missed quarterly payments come with real financial consequences. Build reminders into your calendar or work with a professional who handles this for you.

Mixing personal and business finances. Keep a separate business bank account. Blurring the line between personal and business spending increases your audit risk and makes it much harder to substantiate your deductions.

Operating as a hobby. If you report a net loss for 3 or more years out of a 5-year window, the IRS may reclassify your business as a hobby — stripping away your deductions and taxing your full gross income. Maintaining an LLC and a professional business structure helps protect you here.

Ignoring gifted products. If a brand gifts you a product in exchange for content (a barter arrangement), the fair market value is taxable income and must be reported. Products given with no strings attached generally don’t count as income.

12. FAQ

Do I qualify as self-employed for tax purposes?

Generally, yes — if you earn income outside of a traditional W-2 job, the IRS considers you self-employed.

What if I earn income from multiple platforms?

You must report income from all sources on your Schedule C.

Can I deduct expenses from before I started making money?

Some startup costs are deductible even if they occurred before you started earning. Specific rules apply, so consult a tax professional.

Do I need to pay taxes on gifted products?

Only if it’s a barter arrangement (product exchanged for content), gifts with no strings attached are generally not taxable.

What if my net income is negative?

You won’t owe taxes for that year, but you still must file a return. Be cautious of operating at a loss too frequently (see the hobby classification risk above).

Do I need to file a separate business tax return as an LLC?

No — single-member LLCs file taxes as part of their personal return using Schedule C. Only S Corps require a separate business filing (Form 1120-S).

Conclusion

Paying taxes as a content creator is inevitable once you start making money — but that doesn’t mean you should pay more than your fair share. With the right structure (an LLC, a dedicated business bank account, and consistent bookkeeping), a solid understanding of your deductions, and a handle on your quarterly payments, taxes become a manageable — even empowering — part of running your business.

If you’re paying taxes, it means your brand is growing. The goal is simply to keep as much of that hard-earned income as possible.

Have questions or want help with your creator taxes? Book a call with Cookie Finance today — we only work with influencers and content creators, and we’d love to help you take control of your finances.